In previous writings I have alerted you to the sequence of events that follows the bubble of greed. Let’s review the cycle. It all started in the 1980’s. First, the economic system is growing at a slow and reasonable rate. The Federal Reserve Bank (Fed) is expanding money supply at 3 to 4% to accommodate growth and expansion. Fundamental principles of borrowing and lending are adhered to by both sides of the equation. Chairman Paul Volcker had whipped inflation by raising interest rates into double digits. This put the country into a recession. The cleansing took place and all of the unproductive ventures were pruned from the system. Ronald Reagan decided to reduce government and began to privatize. The practice of defined benefit plans where the company supplies the worker with a pension was being dismantled. IRA’s and 401K’s replaced those defined benefit plans. The average Joe was expected to invest and produce a return equal to professional money managers. The 80’s produced an unprecedented number of new investors. New brokerage firms sprang up. With the maturity of the internet, electronic brokerage firms flourished. A new era began- technical trading. In its early years, technical trading was accomplished by a specialized broker who set up multiple workstations in a trading room. Traders would use charts and graphs to pick entry and exit points. It worked for a while. As more traders began to use technical analysis, the "big boys" with their high powered black boxes could determine what trading indices and formulas most traders were using. Once they figured it out, they would set traps for the trading population. They would force a stock up and lure traders in then sell it short and force the traders to take a loss. Stocks are a zero sum game, a winner and a loser on every transaction.

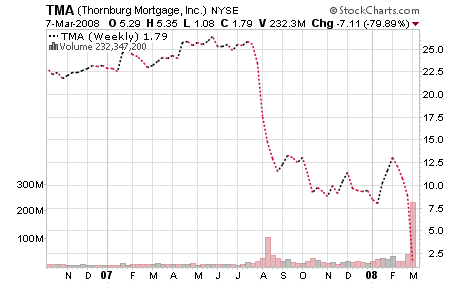

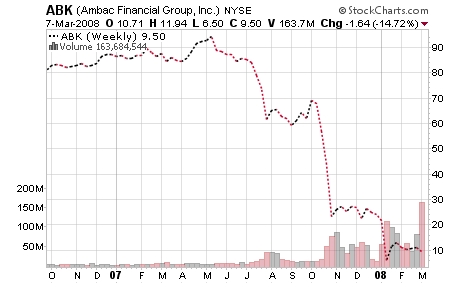

The Big Boys are playing a game of perception. The global financial economy needs to contract and de-leverage the excesses of investing that has occurred over the last 20 years. Alan Greenspan will be found to be the perpetuator of this leveraging problem. Most of the problem happened on his watch. Bill Clinton’s era is where most of it started. George Bush perpetuated it as well. Big money wanted to keep the party alive. Unchecked greed propelled this problem into the stratosphere. U.S. Treasury Secretary Henry Paulson looks like an orchestra conductor. Wall Street is the audience. The average money manager is deep within the current paradigm. The pension fund manager inherently believes that his portfolio will weather any short term problems. His portfolio is designed to look out 50 years, not 50 months. As long as Paulson can keep these people believing that all is well, the market may maintain a sideways movement. However the chickens will come home to roost.

I view this time as a great time to add to your portfolio of hard assets. With the recent $160 drop in the price of gold, I see this as a buying opportunity. I hope that they can manipulate the price of gold to stay at this level for a number of months. That will allow me to buy more gold and silver stocks as I can afford. Energy prices remain strong. The energy stocks have responded accordingly.

I believe the 15% drop in gold was orchestrated to settle down the markets. Remember, gold is a barometer against the fiat currency health. Gold goes up when the US dollar goes down. It will be choppy ahead. Rest assured that the powers that be will do everything necessary to "stay alive".

Some questions we have recently received:

Would you acquire the presidential coins that are being offered now in the newspapers or is this just a perception based offer? No, I wouldn’t pay a premium for coins based on their rarity.

“I am not suggesting to hoard gold or silver.”

The quote above suggest to me that you are not investing in Silver any longer to protect yourself against the weak dollar. I took your advice in Oct 2003 and put all my cash into real silver. Do you now believe we should not do this now? My comment refers to the time when the possible collapse of the dollar. At that time you should look to help people with the wealth you have acquired from my counsel. Hoarding denotes fear. Your current continued acquisition is based on a future need. In Genesis, Joseph acquired assets for a future need. Once the need was there, the assets were there to help others. We’re doing the same thing. Gold and silver are simply "tools", not to be worshipped.

I have a question about buying silver. We have about $50K invested with E**** Jones because we know nothing about finances except there never is enough, and we were wondering what percentage of that 50K would be reasonable to buy silver rounds. And mostly, why? This is my wife’s idea and I do want to honor her. I would own about $5,000 in silver rounds. I would also consider buying a little each month. In my investment account I would check to see exactly what the 50K is invested in. I have invested in Chevron, Petrohawk, Pennwest Energy, Goldcorp, Yamana Gold, Southern Copper, etc. See Disclaimer on the website.